On 2 June 2026 the United Kingdom switched on its first new payment scheme since Faster Payments launched in 2008. The UK Payments Initiative (UKPI) went live with a commercial variable recurring payments (cVRP) scheme — a way for businesses to take flexible, recurring bank-to-bank payments that a customer has explicitly authorised. For any company that bills customers or sells online, this is the moment “pay by bank” stops being a sweeping curiosity and becomes a real alternative to Direct Debit and card-on-file. The software question follows immediately: is your checkout, billing, and reconciliation stack ready to offer it?

What actually went live

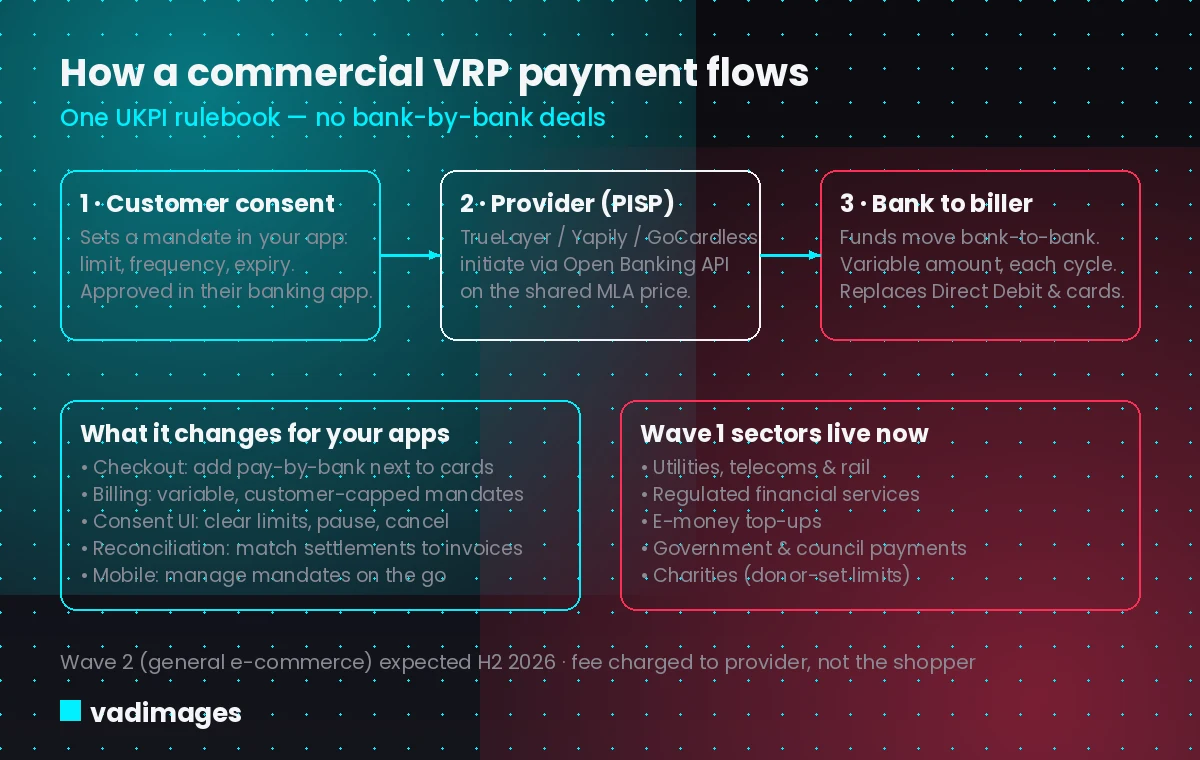

Variable recurring payments already existed in a limited form. Since 2022–2023, “sweeping” VRP let people move money between their own accounts automatically and for free. Commercial VRP extends that same consented, customer-set mandate to paying third parties — utilities, regulated financial firms, government, and charities. The customer approves a mandate in an app once, setting a maximum amount, a frequency, and an expiry, and from then on a payment provider can initiate variable charges within those limits without re-prompting for every transaction.

The piece that makes this work at national scale is UKPI itself: an independent, industry-owned company that publishes a single rulebook and a shared commercial model. Thirty-one firms funded and established it, deliberately mixing the banks that build the rails with the fintechs that initiate payments — named participants include Nationwide, NatWest Group, Mastercard Open Banking Services, GoCardless, TrueLayer, Yapily, Token.io, Moneyhub and Plaid. Because every participant transacts on the same terms, providers no longer negotiate bank by bank. Regulators set a target of roughly 75% of UK current accounts being reachable at launch, the critical mass needed for the scheme to be useful.

Why fintech and finance teams should care

The commercial model is the headline for anyone doing the maths. Instead of percentage-of-value card fees, cVRP is built around a Multilateral Agreement: a centrally managed, single fixed pence-per-transaction fee, charged to the payment provider rather than the shopper. The cost modelling behind it put a bank’s per-transaction cost at around £0.02 plus a scheme fee, and the price is intended to stay fixed for roughly five years to give merchants cost certainty. In January 2026 the FCA and PSR signalled they would not, at this stage, prioritise a Competition Act investigation into that centralised pricing, giving the scheme interim regulatory comfort to proceed.

For high-volume billers and fintechs, a flat, predictable per-transaction cost on recurring revenue is materially different from blended card economics. It also changes the customer relationship: a cVRP mandate is consented, capped, and easy to pause or cancel, which can reduce disputes and failed-payment churn compared with cards that expire or Direct Debits that are hard to vary.

Wave 1 now, e-commerce next

UKPI is rolling out in waves. Wave 1, live now, deliberately starts with lower-risk, trusted sectors:

- Utilities, telecoms and rail — energy, water, broadband and transport bills with variable monthly amounts

- Regulated financial services such as mortgage servicers and pension administrators

- E-money institutions, for topping up wallets and accounts

- Central and local government payments, such as council tax and fees

- Registered charities taking recurring donations with donor-set limits

Wave 2, expected in the second half of 2026, opens the scheme to general e-commerce. That sequencing matters for planning: if you operate in a Wave 1 sector you can adopt now, and if you sell online you have a concrete window to get your checkout and subscription flows ready before the broader launch.

The build work this creates

Commercial VRP is delivered through software, and the experience lives in the screens your customers actually use. A pay-by-bank option has to sit cleanly next to cards at checkout, a mandate-setup flow has to show limits and frequency in plain language, and customers need a self-service place to view, pause, or cancel what they have authorised. Behind that, settlements arriving as bank credits need to be matched back to invoices and subscriptions so finance teams are not reconciling by hand. None of that is hardware or advice — it is web and mobile interface work plus integration against open banking APIs.

How Vadimages helps

Vadimages builds the web and mobile software that turns a scheme like cVRP into something your customers can use. On the front end, that means adding a pay-by-bank path to your existing checkout or building a subscription and billing portal where customers set, review, and manage their mandates — with clear caps, pause, and cancel controls — on the web and in a companion mobile app. On the integration side, we build the API layer that connects your storefront, portal, or internal tools to your chosen payment-initiation provider (for example TrueLayer, Yapily, or GoCardless) through clean REST or GraphQL services, so the provider can be swapped or added to without rewriting your product.

We also build the operational surfaces around payments: reconciliation and reporting dashboards that match incoming bank settlements to invoices, flag failed or out-of-limit mandates, and give finance and support teams a single screen to work from. Vadimages does not operate your banking rails or act as a payments provider, and we do not give regulatory or financial advice — we deliver the websites, web apps, customer portals, dashboards, integration layers, and mobile apps that make a new payment option a usable part of your product.

Bottom line

Commercial VRP is live, priced, and backed by the banks and fintechs that have to make it work. Wave 1 sectors can adopt today; online sellers have until the second-half Wave 2 launch to prepare. The differentiator will be the software experience around it — the checkout, the mandate management, the reconciliation — and that is exactly the web and mobile layer worth getting right now. This article is general information, not legal, financial, or regulatory advice.