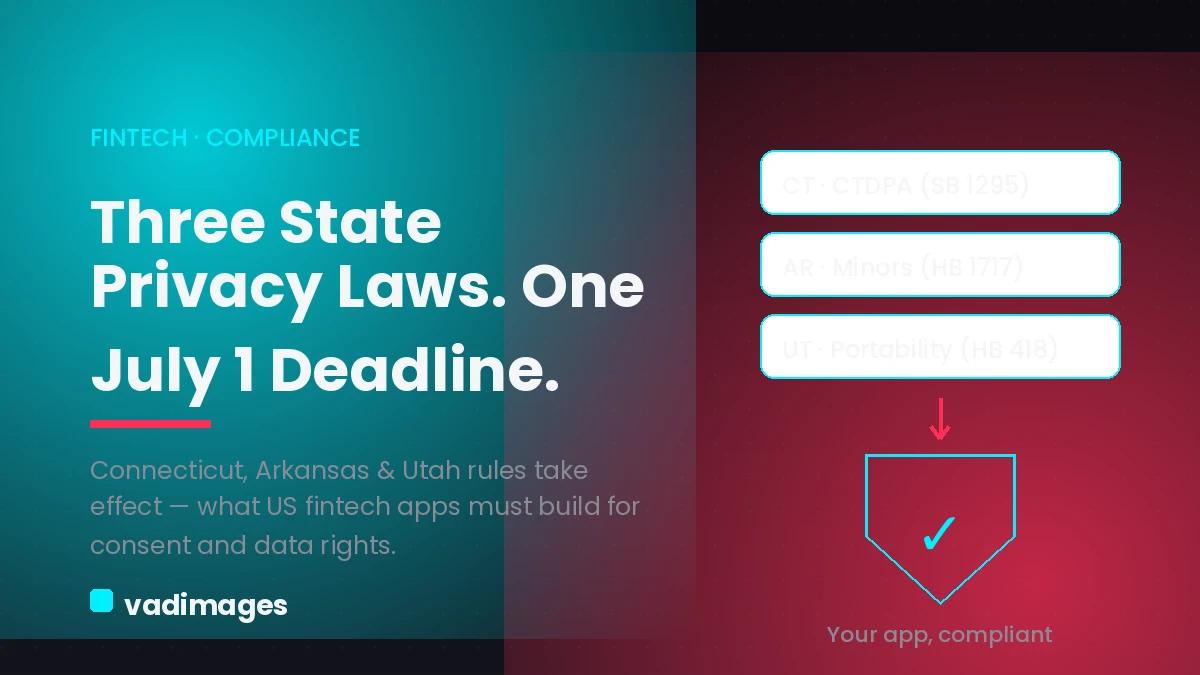

Today draws a real compliance line for a lot of US software teams. On July 1, 2026, three state privacy measures take effect at once — amendments to Connecticut’s Data Privacy Act (SB 1295), Arkansas’s Children and Teens’ Online Privacy Protection Act (HB 1717), and updates to Utah’s Consumer Privacy Act (HB 418). For fintech and financial-services companies running consumer-facing web and mobile apps, the Connecticut changes are the ones to read closely, because they quietly dismantle an exemption many financial firms have leaned on and pull far more of their data into scope.

What changed on July 1

Three separate laws share the same effective date. Connecticut amended its comprehensive privacy act to broaden coverage, expand what counts as sensitive data, and add new disclosure duties. Arkansas turned on a dedicated regime for online services directed to minors, with a tiered consent model and a ban on targeted advertising to children and teens. Utah added new social-media data portability and interoperability rights, giving consumers more control over moving their data between platforms. Together they continue a pattern US businesses now know well: there is no single federal privacy law, so obligations arrive state by state, and the practical work of complying with them lands in your product and your codebase.

Why Connecticut is the one fintechs should read

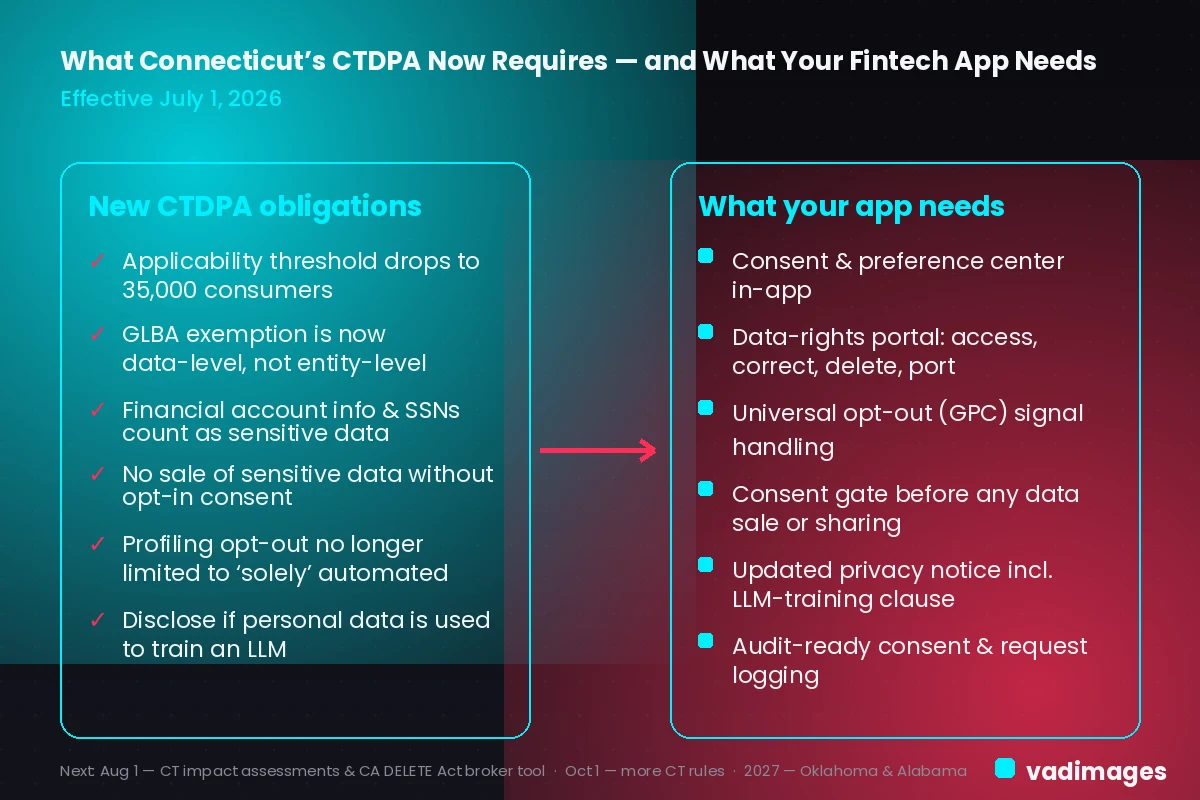

Many financial companies have treated privacy compliance as someone else’s problem because they are regulated under the federal Gramm-Leach-Bliley Act (GLBA). Connecticut just made that assumption dangerous. The amendments replace the old entity-level GLBA exemption with a narrower data-level exemption. In plain terms, being a GLBA-regulated business no longer puts your whole organization out of scope; only the specific data actually covered by GLBA is exempt. Everything else — marketing databases, prospect lists, website and app behavioral analytics, and data from products that sit outside your GLBA-regulated activities — is now squarely inside Connecticut’s law and needs a careful, data-by-data review.

The rest of the Connecticut package compounds the effect for anyone handling financial and identity data:

- The applicability threshold drops from 100,000 to 35,000 consumers, pulling many smaller fintechs and financial apps into coverage for the first time.

- Coverage is no longer purely volume-based: any organization that processes sensitive data or sells personal data is in scope regardless of how many consumers it touches.

- The definition of sensitive data now expressly includes financial account information, Social Security numbers, government-issued identifiers, neural data, and certain biometric or genetic data.

- Sensitive data cannot be sold without the consumer’s consent — an opt-in gate, not a buried opt-out link.

For a consumer fintech app, that combination means the data you handle every day — linked bank accounts, SSNs collected for identity verification, device and behavioral signals — is exactly the data the law now treats as most sensitive.

The AI clause every fintech should map to its privacy notice

Two Connecticut provisions speak directly to how fintechs use automation. First, there is a new disclosure obligation: if you introduce personal data into the training of a large language model, you must say so. For firms building AI-powered support agents, underwriting assistants, fraud models, or personalization features on top of customer data, that is a concrete privacy-notice update, not an abstract policy question. Second, the profiling opt-out is expanded by removing the old limitation that a decision be based solely on automated processing. A human being nominally in the loop no longer takes a consequential, profiling-driven decision outside the consumer’s right to opt out — which matters for any app that ranks, scores, or segments customers to drive an outcome they care about.

A wave, not a one-off

Connecticut, Arkansas, and Utah are one crest of a longer wave, and the calendar behind them is unforgiving. Arkansas’s minors law sets a two-tiered consent framework — parental consent for children twelve and under, and consent from either the teen or a parent for users thirteen to sixteen — while prohibiting targeted advertising based on minors’ data and limiting what can be collected and retained. Utah’s portability and interoperability rules push platforms to let users move their data more freely. And more is already scheduled: on August 1, 2026, Connecticut’s data-protection impact-assessment obligations begin for high-risk processing, and California’s DELETE Act data-broker deletion mechanism becomes fully operational; additional Connecticut amendments follow on October 1, 2026; and comprehensive laws take effect in Oklahoma on January 1, 2027 and Alabama on May 1, 2027. If your app serves customers across state lines — and most fintechs do — you are building for a moving target of overlapping requirements, which is exactly why the compliance logic belongs in reusable product infrastructure rather than one-off patches.

How Vadimages helps

Complying with these laws is, in practice, a web and mobile engineering project: the obligations turn into screens, flows, APIs, and logs inside your product. As a custom web and mobile app development studio, Vadimages can:

- Build a consent and preference center into your web and mobile app, with an opt-in gate before any sale or sharing of sensitive data such as financial account information or SSNs.

- Ship a data-rights portal so consumers can exercise access, correction, deletion, and portability requests, backed by a workflow that routes, tracks, and fulfills them within statutory deadlines.

- Implement universal opt-out signal handling — including Global Privacy Control — on your marketing site and in-app, so honored preferences propagate consistently across surfaces.

- Add profiling and automated-decision opt-out controls that reflect Connecticut’s broader standard, plus the privacy-notice updates that disclose any use of personal data to train large-language-model features.

- Instrument audit-ready consent and request logging, so you can demonstrate what a consumer agreed to, when, and how a request was handled.

- Put each state’s rules behind a configurable policy layer in your own backend, so a new state effective date — Oklahoma, Alabama, or the next amendment — is a configuration change rather than a rebuild.

Everything here stays on the web and mobile software side. Vadimages builds the product infrastructure that makes compliance operational; we do not provide legal, tax, or financial advice, and your obligations should be confirmed with qualified counsel.

Bottom line

The July 1, 2026 privacy changes are not a one-line policy edit. Connecticut’s move from an entity-level to a data-level GLBA exemption, its lower 35,000-consumer threshold, and its treatment of financial account data and SSNs as sensitive data mean far more of a fintech’s everyday data is now regulated — and the consent, data-rights, and disclosure duties all resolve to features you have to build and prove. Treat it as a prompt to make consent, data-rights fulfillment, and universal opt-out signals first-class parts of your app, architected to absorb the next state deadline instead of scrambling for it.

This article is for general information only and is not legal advice; confirm your specific obligations with qualified counsel.